- Washington has a unique capital gains tax despite having no state income tax. Understanding how the system works is essential for investors and business owners who may be affected.

- Not all assets are treated the same under Washington’s tax rules. Certain gains are taxable while others are specifically excluded, which can significantly impact tax outcomes.

- Planning ahead can make a meaningful difference. The way and timing of asset sales can influence how much tax you ultimately owe.

Although Washington is one of a few states without a traditional state income tax, the state implemented a state capital gains tax in 2022, which was upheld despite a repeal vote in 2024.

This unique tax on certain long-term capital gains has important planning implications for Washington residents, particularly those with sizable investment portfolios or business ownership interests.

The Washington capital gains tax has several features that make it unlike any other state’s tax system.

What is the Washington State Capital Gains Tax?

Defining Capital Gains

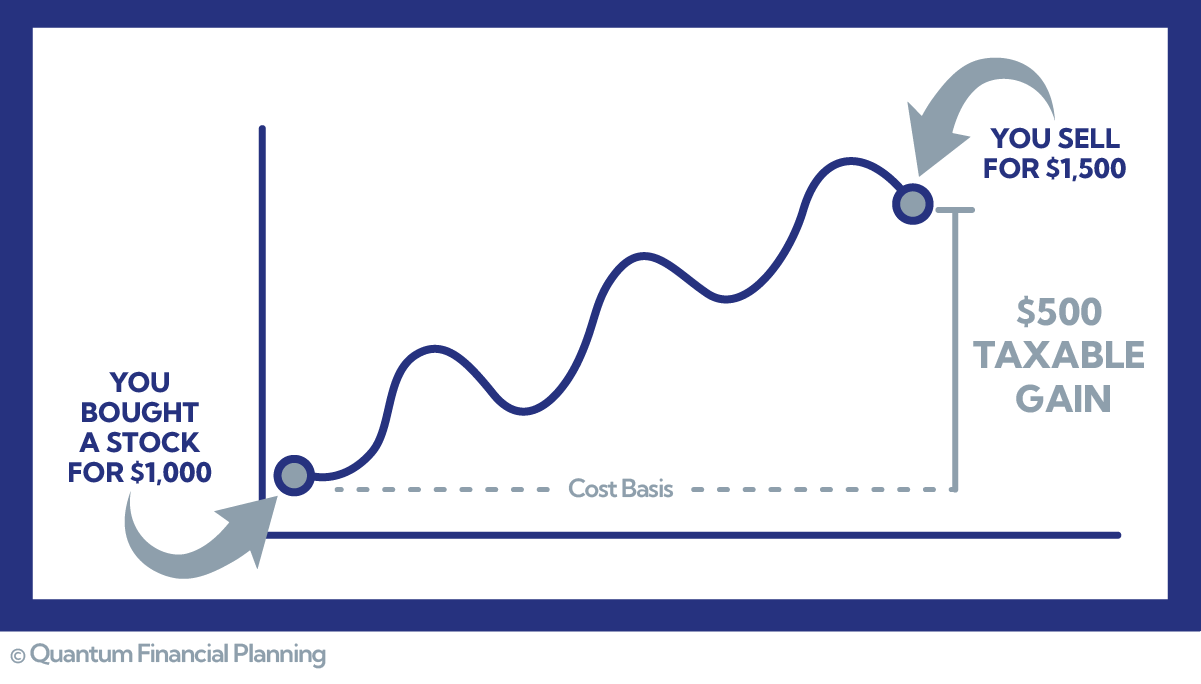

A capital gain is the profit you make when you sell something for more than you previously paid for it. It’s the difference between the price you sell it for and the price you paid.

For example, if you bought a stock for $1,000 and later sell it for $1,500, you have a capital gain of $500.

Context for the Washington Capital Gains Tax

The IRS has taxed capital gains since 1913, but Washington’s tax is more recent. Originally enacted in 2022, the tax was challenged but ultimately upheld by the state’s supreme court in 2023, and survived a vote to repeal in 2024.

In contrast to the federal system, Washington does not tax wages, salaries, or retirement income at the state level. The state instead relies on a more nuanced tax structure, which includes sales taxes as well as both a state capital gains tax and a state estate tax.

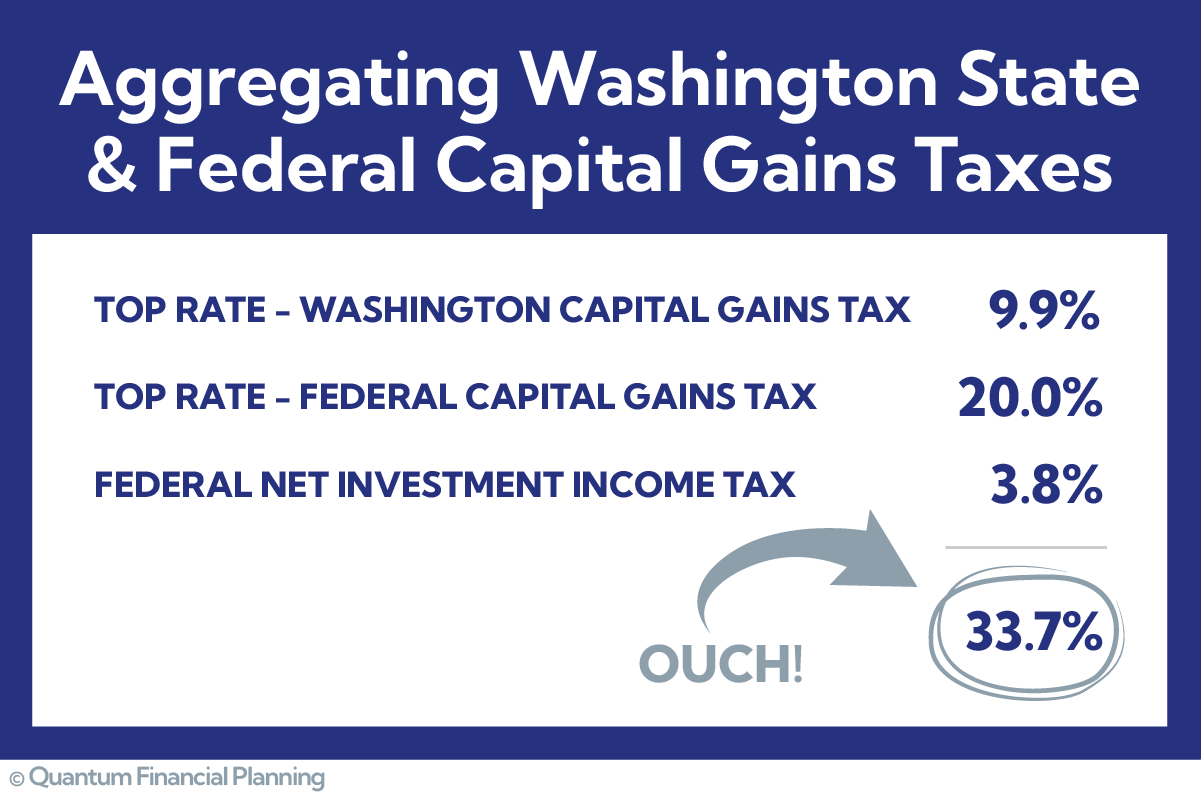

The state capital gains tax is assessed on top of the federal capital gains tax, which makes it costly for Washington residents to sell appreciated assets without proper planning.

How Washington Taxes Capital Gains

Washington Capital Gains Tax Rates

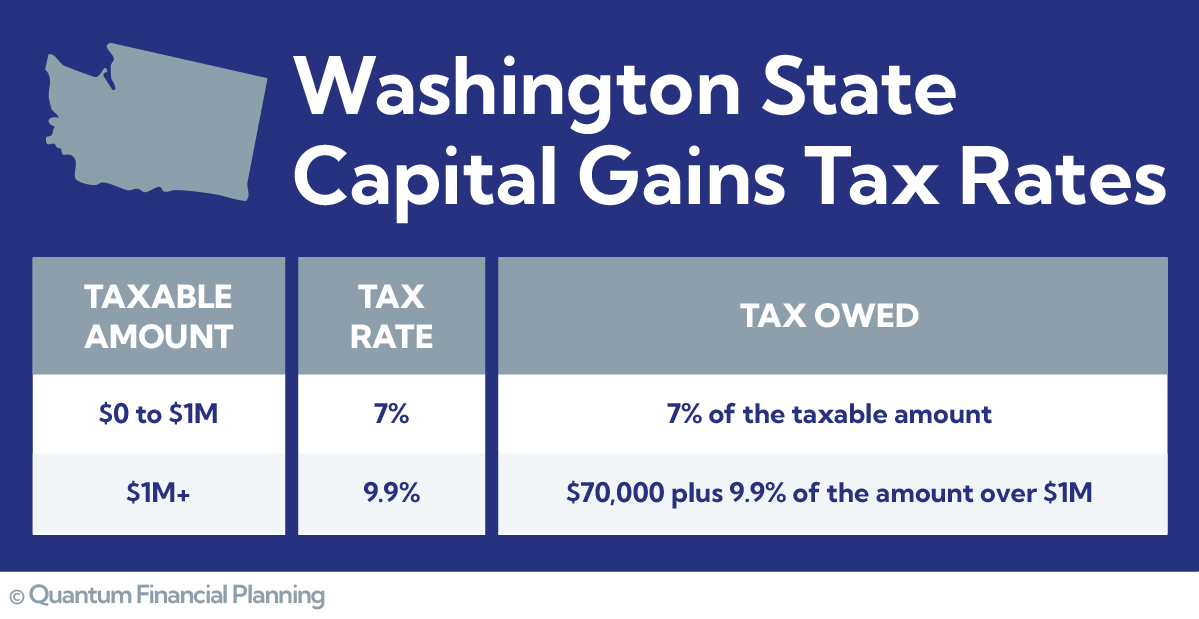

Beginning in the 2025 tax year, Washington applied a tiered (or progressive) tax rate structure to capital gains.

The state’s standard deduction is indexed for inflation each year, providing taxpayers with a substantial “tax-free” threshold before any Washington capital gains tax applies. In practice, this means many residents owe no state capital gains tax unless their long-term gains are significant.

For those with long term capital gains over that threshold, the tax rate starts at 7% and climbs to 9.9%.

Who is Subject to the Washington Capital Gains Tax?

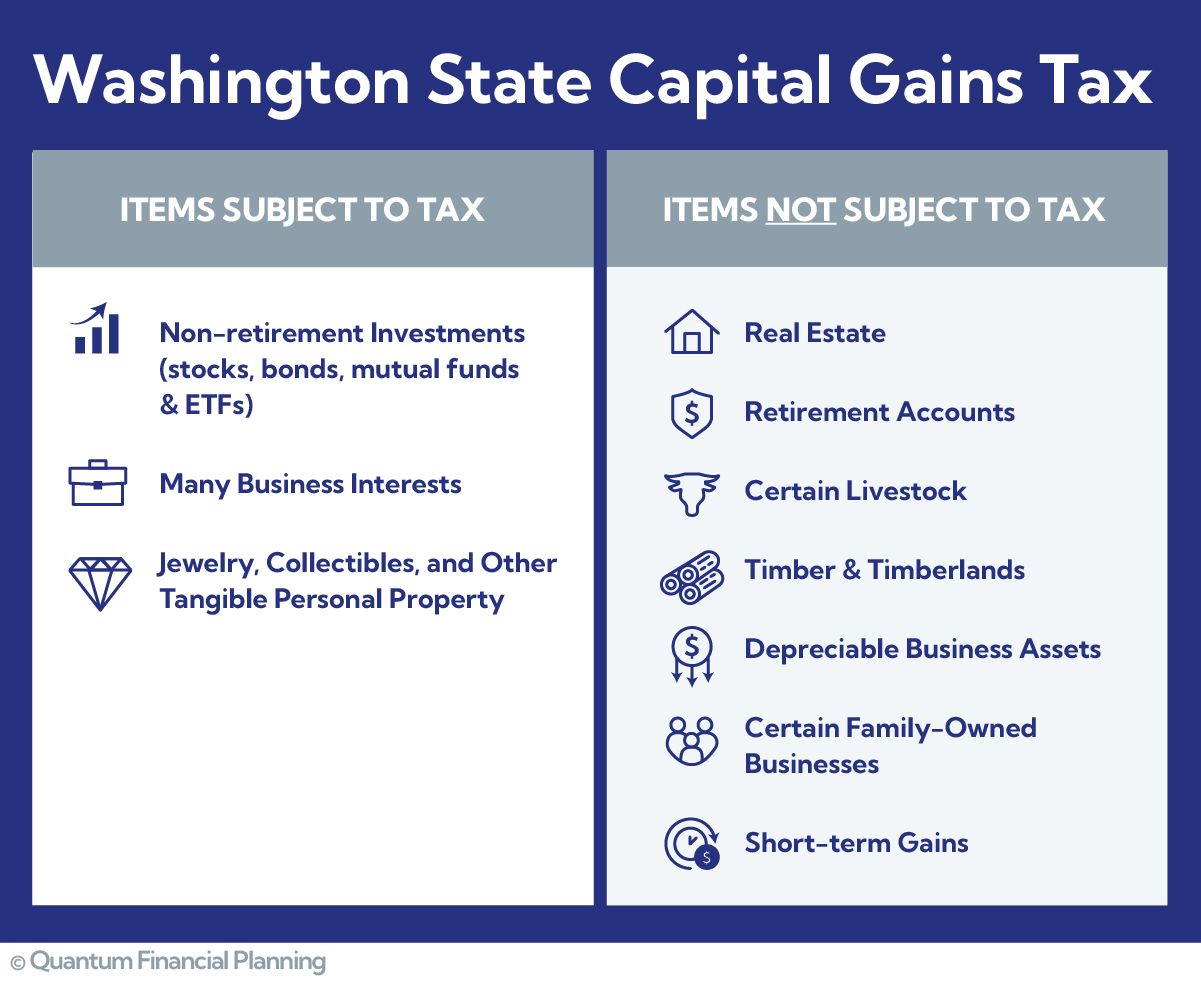

The Washington capital gains tax applies primarily to Washington residents selling appreciated financial assets (think: stocks, bonds, mutual funds, and ETFs) as well as certain tangible assets (think: collectibles or antiques).

However, certain non-residents may be subject to the tax if they sell tangible personal property inside the state or if they own a pass-through entity that has a taxable gain in Washington.

Which Capital Gains Are Subject to the Tax?

Long-Term Gains Only

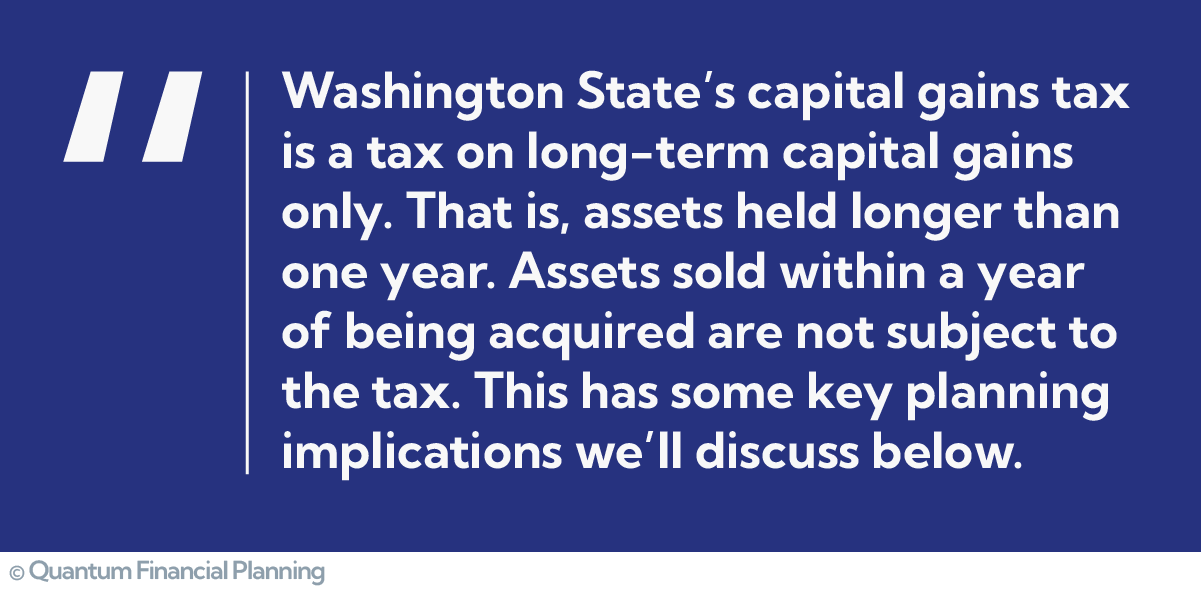

As noted above, the Washington state capital gains tax applies only to long-term capital gains on the sales of assets held longer than one year.

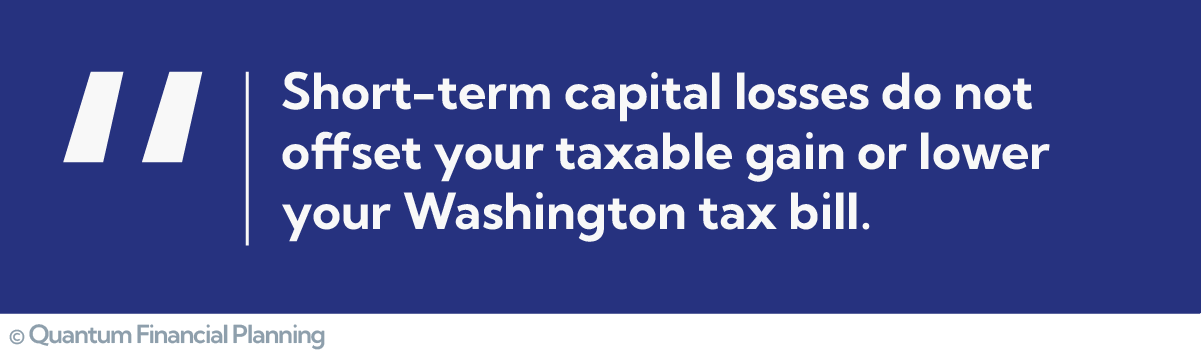

While this means short-term gains are not subject to the tax, it also means short-term capital losses do not offset your taxable gain or lower your Washington tax bill.

Common Taxable Assets in Washington State

Stocks, Bonds, Mutual Funds, and ETFs

Non-retirement investment assets are one of the most common sources of taxable gains in Washington. If your brokerage account has been on a good run, you’ll want to consider WA tax implications before selling.

Business Interests

Many private business sales will also trigger capital gains taxes in Washington as the Washington capital gains tax applies to both outright sales as well as sales of minority interests.

There is an exception, however, for Qualified Family-Owned Small Businesses (QFOSB). See detailed discussion below.

Tangible Personal Property

An often overlooked asset type that shouldn’t be ignored for tax purposes is tangible personal property.

This includes items such as high-value collectibles, such as art or antiques, as well as “lifestyle assets” such as yachts and other boats, planes, or collector cars.

Jewelry and precious metals such as gold bars or silver coins would also be considered taxable personal property in Washington state.

Selling tangible personal property at a profit is a rare occurrence for most. If you’re considering liquidating a collectible or a family heirloom, it’s critical to plan ahead so as to not trigger unnecessary taxes on other assets or investments you may hold.

Note for Non-Washington Residents

A sale of tangible personal property that occurs in the state of Washington can trigger WA capital gains tax for the seller, even if they live in another state.

Which Capital Gains Are Exempt in Washington?

Real Estate Sales

Real estate is specifically excluded from the Washington capital gains tax. This includes single family, multi-family, commercial, and land properties.

This is a major difference between Washington’s tax and the federal capital gains tax.Real estate is not exempt from federal taxes, though exclusions do apply for the sale of your primary residence.

Retirement Accounts

Washington state does not tax capital gains on assets held in qualified retirement accounts.

Gains from investments held in 401(k)s, 403(b)s, IRAs, and all other qualified retirement accounts are exempt and can be ignored for tax purposes.

This is also true for federal capital gains taxes.

Agricultural Assets

In addition to farmland being exempt due to the real estate exemption mentioned above, the Washington tax has two more ag-related exclusions.

Gains from the sale of certain livestock related to farming or ranching and gains from the sale or exchange of timber and timberlands are exempt from the tax.

Depreciable Business Assets

Assets used in a trade or business that are depreciable under federal tax law are also exempt from the state capital gains tax.

Think machinery, equipment, vehicles, and furniture used in a business as common examples. If you are selling an interest in a small business, careful planning is required to accurately allocate the portion of the sale price that can be attributed to such property.

Qualified Family-Owned Small Business (QFOSB) Deduction

Although many sales of business interests in Washington result in capital gains taxes, there is a specific carve-out for Qualified Family-Owned Small Businesses (QFOSB).

To qualify for this deduction, the following must be true:

- You must have owned an interest in the business for at least five years prior to sale

- You and/or a member of your family must have materially participated in business operations for at least five of the last ten years

- The business had gross revenue of less than the established gross revenue limit ($11.095 Million in 2025, indexed to inflation) in the last 12 months

- The business must be either: At least 50% owned by you and your family, or at least 30% owned by you and your family and 70% owned by no more than two families or 90% by no more than three families

Other Exemptions

Washington’s department of revenue lists a couple of additional exemptions that are very specific (and quite rare): commercial fishing privileges and goodwill received from the sale of a franchised auto dealership.

If you think either of these might apply to you, connect with a tax advisor to plan ahead of a potential sale.

Understanding Federal Capital Gains Tax

Short-Term vs. Long-Term Capital Gains

Unlike the state of Washington, the IRS taxes both short-term and long-term capital gains.

The Federal system actually imposes higher rates on short-term gains, which are excluded from Washington’s tax entirely, than it does on long-term gains. Short-term gains are taxed at your ordinary income tax rate (10%-37%) while long-term gains are taxed between 0% and 20%.

📊 View Our 2026 Federal Tax Guide → See the current federal tax brackets, including updated income thresholds for both ordinary income and long-term capital gains.

This is a key difference between the federal system and Washington’s tax, as it has major planning implications.

For federal tax purposes, short-term losses can be used to offset long-term gains. So, if you have a gain from the sale of an investment you held longer than a year, but stocks you bought within the last 12 months are trading at a loss, you can sell those stocks to take the loss and decrease your total taxable gain.

Because Washington does not tax short-term gains, however, short-term losses can not be used to decrease a tax bill associated with a long-term gain. This limits your ability to reactively plan around your tax bill, emphasizing the importance of proactive planning.

Net Investment Income Tax

In addition to the federal taxes referenced above, the IRS assesses a 3.8% Net Investment Income Tax (NIIT) on investment income for high earners.

This means Washington taxpayers could be paying over 33% in combined taxes on long-term capital gains!

Capital Gains on Real Estate: Why Washington is Different

Unlike Washington, where the state specifically exempts all real estate transactions from its capital gains tax, the federal tax does apply to most capital gains on real estate.

If you own a rental property or a vacation home that has increased in value, you could be on the hook for federal taxes when you sell it.

Primary Residence Exclusion

That being said, the IRS does offer an exemption for your primary residence. Under current law, the first $250,000 in gains on the sale of your primary home is tax-free ($500,000 for a married couple).

How To Calculate Capital Gains Tax in Washington

Determine Basis

For investments like stocks, bonds, mutual funds, and ETFs, this is pretty easy. Your basis is the price you paid when you bought the investment. If you were gifted or inherited the asset, it gets a little bit more complex but shouldn’t be too hard to find.

For business interests and other unique assets, tracking basis can get pretty complicated, but a good CPA should be able to help you track it down.

Reminder: we’re only considering assets owned for more than one year when calculating the Washington state capital gains tax.

Determine Long-Term Gains

Once you have an accurate basis, determine the amount of gains by subtracting your basis from the price you received upon the sale.

Keep in mind, if you incurred fees to sell an asset (such as a broker fee or similar), those fees reduce your capital gain.

Apply State Deductions and Exemptions

Make sure to exclude any gains from exempt transactions listed above.Reduce your total gain by the current Washington state standard deduction ($278,000 in 2025).

Apply Tax Rate

If your total taxable gain is below $1M, multiply your gain by 7% and you’re done.

Apply Tiered Rate for Taxable Gains over $1,000,000

For gains over $1M, multiply the first $1 million by 7% ($70,000) and the remaining amount by 9.9%.

Strategies to Reduce Washington and Federal Capital Gains Taxes

Strategic Timing

For those who own assets with significant unrealized gains, spreading out the sale over multiple tax years can go a long way towards avoiding the Washington state capital gains tax.

For example, assume you retire with $2,000,000 of your employer’s stock with a basis of $500,000. You have a gain of $1.5M. Instead of selling it all in a single tax year to diversify, you may want to consider selling $270,000 each year until it’s diversified.

This will keep you under the taxable threshold in Washington and avoid paying unnecessary taxes. Now keep in mind, there may be risk involved in staying heavily concentrated for longer to avoid taxes.

Installment Sales

If you’re selling a business or another more complex capital asset, consider structuring it as an installment sale to spread the taxable gain out over the life of the contract.

Donating Appreciated Assets to Charity

If you’re charitably inclined or giving is a goal of yours, develop a tax-efficient giving strategy.

Instead of writing a check to your favorite charity, consider asking them to help facilitate the transfer of appreciated stock. This can help you to avoid both federal and state capital gains taxes.

If transferring stock directly is difficult, opening a Donor-Advised Fund can help to maximize the tax benefits of a charitable gift.

Gift Appreciated Stock to Family Members

Giving stock away to family members is generous. That said, if your family member is in the same income tax bracket as you, it might not save much in total taxes.

This strategy works best if, for example, a grandparent in a high tax bracket with significant capital gains gives some of their stock to a grandchild in a low tax bracket with far less capital gains.

When giving stock away, the recipient inherits your basis (and therefore your unrealized gain). So, if your friend or family member is below the Washington capital gain threshold, having them sell it instead of selling it before you give them money is ideal.

Proactive Estate Planning

Appreciated assets get a step-up in basis upon your death. If you’re planning to leave assets to future generations, prioritize passing assets down with significant gains.

This will help avoid taxes and maximize the amount your heirs receive.

For more on proactive estate planning in Washington state, take a look at the following articles:

- Washington State Inheritance Tax: A Comprehensive 101 Guide

- Washington Estate Tax: Everything You Need to Know

Washington Capital Gains Tax FAQs

Is the Washington capital gains tax still being challenged in court?

Not currently. The Washington Supreme Court ruled in March 2023 that the state tax is indeed constitutional. Furthermore, in 2024, the U.S. Supreme Court refused to hear an appeal challenging the Washington court’s decision.

How does the Washington capital gains tax apply to cryptocurrency?

The sale of cryptocurrency is a taxable event when it comes to Washington’s capital gains tax. Assuming the crypto asset is held for longer than one year (long-term) and gains breach the state standard deduction threshold, you will have tax due.

What happens if I move out of state before selling an asset?

Moving out of state can definitely help avoid some Washington state taxes, though there are other factors to consider in such a move.

For intangible assets or financial assets like stocks and bonds, you will not owe Washington capital gains tax on the sale if you establish domicile in another state and no longer maintain a home within the state. Timing matters here. You must move prior to selling the asset and maintain clear records.

For physical assets (such as collectibles), Washington taxes can be avoided if the asset being sold was not located in Washington at the time of sale or during the current or preceding calendar year. This also assumes you establish a domicile in another state prior to the sale.

How do I report capital gains in Washington and pay the tax?

Information on how to file a Washington state capital gains tax return and how to pay taxes due can be found on the Washington Department of Revenue website.

Do I owe this tax if I sell a rental property?

No. Real estate transactions are specifically exempt from the Washington state capital gains tax.

Are trusts or estates subject to the Washington capital gains tax?

It depends. The Washington state capital gains tax is explicitly a tax on individual taxpayers. Therefore, trusts and estates avoid the Washington tax for the most part.

However, certain trusts like a revocable living trust are treated the same as the individual grantor and, as such, could be subject to the tax.

Can capital losses offset Washington state capital gains?

Yes, but you can only use long-term losses to offset long-term gains in Washington. If you have stocks that you have held for longer than one year and they are trading at a loss, selling your shares could help offset taxable gains elsewhere.

We often meet with folks who are frustrated to learn that they can’t use short term losses to offset long term gains, however.

We Help Washington Residents Plan Around Capital Gains

Though Washington does not have a state income tax, the state’s tax system has become increasingly complex. Without proper planning, the state could be getting more of your nest egg than you’d like.

Our Washington-based team has extensive experience navigating these complexities.

We can help guide you through your retirement tax-efficiently so you can enjoy what’s next.

Schedule a call with our team.