Moving to Washington for Retirement? A Tax and Estate Planning Checklist Before You Change Residency

By Nick Fuller, CPA, CFP®

Key Takeaways:

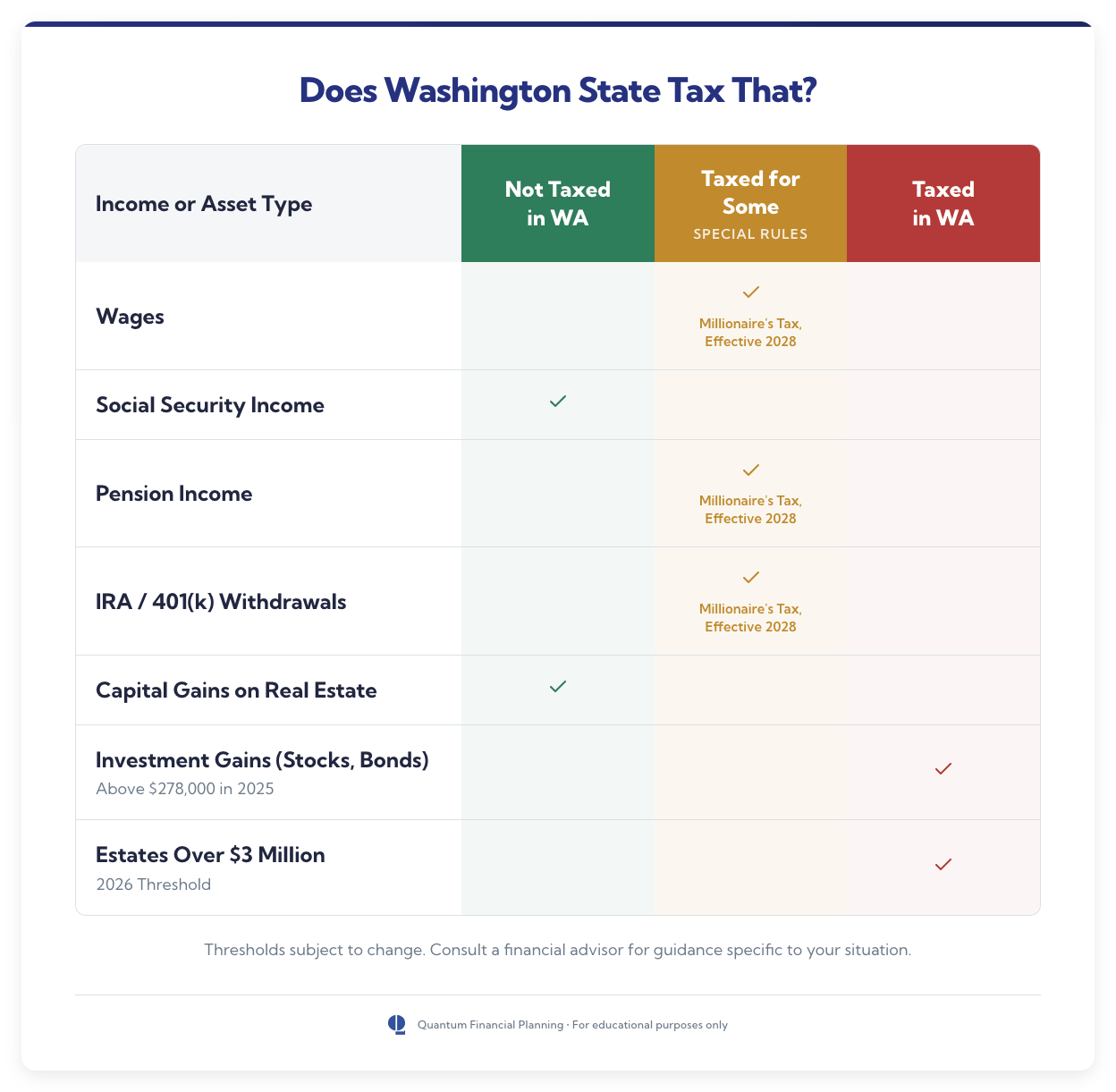

Washington has no state income tax on wages, Social Security, or pension income, but does have its own estate tax (separate from the federal estate tax) and capital gains tax that may impact retirees with significant assets.

Changing your state of residence involves more than updating your address. Establishing Washington state as your domicile requires documented intent, reducing ties to your former state, and careful timing of major financial decisions.

Estate planning documents are state-specific. Moving to Washington is a good time to review and update your will, trust, powers of attorney, and beneficiary designations with a Washington estate planning attorney.

Washington state’s tax landscape has become increasingly more complicated in recent years. For the majority of residents, however, it remains one of the more tax-friendly places to retire. Wages, Social Security, and pension income aren’t subject to state income tax, and that’s a real draw for a lot of people.

Whether those tax advantages apply to your situation, though, depends on your net worth, your household income, where your income comes from, and how your estate plan is set up. Establishing Washington state as your primary residence — and avoiding tax obligations in both your former state and your new one — takes deliberate planning.

That means getting the timing right on key financial decisions, updating important estate planning documents, and building a paper trail that clearly shows Washington is your state of residence.

When it comes to relocating in retirement, a little advanced planning can go a long way. This tax and estate planning checklist will walk you through some key financial and legal considerations so you can make the move with confidence. Reach out to our team of CERTIFIED FINANCIAL PLANNER® professionals serving clients in Spokane, WA and nationwide if you’re thinking about relocating to Washington state and need help navigating the financial side of your move.

Retiring in Washington State: Key Tax Considerations Before Making the Move

Washington doesn’t have a state income tax on wages, Social Security, or pension income. That’s a plus for many retirees. However, depending on your situation, two other types of taxes could significantly impact your finances if you choose to move to Washington state.

Washington’s Estate Tax

Washington does have an estate tax, and the threshold is lower than you might expect. If Washington is your state of residence in 2026, the tax applies to estates valued above $3 million. That may sound like a lot, but when you add up savings, a home, retirement accounts, and other assets, many retirees cross that threshold without realizing it.

Many married couples think they’re in the clear if their estate is below $6M total ($3M each) but without proper estate planning, the death of one spouse could create a taxable estate for the surviving spouse. By comparison, the federal estate tax threshold is $15 million per person ($30 million for married couples). So many retirees who wouldn’t owe federal estate taxes could still face a tax bill in Washington state.

If your estate is above the Washington state estate tax threshold, that’s something to consider before establishing residency status here.

Washington’s Capital Gains Tax

Washington also taxes profits from the sale of certain long-term investments, such as stocks, bonds, ETFs, and mutual funds (known as a capital gains tax).

The capital gains tax applies to gains that exceed the standard deduction of $278,000 (the 2025 threshold, adjusted annually). Real estate sales are not subject to this state capital gains tax and other exemptions exist.

If you’re planning to sell investments around the time of your move, the timing of those transactions relative to when you establish Washington residency is worth thinking through carefully.

Residency vs. Domicile: What Actually Changes When You Move

When people think about moving to a new state, they often think about the practical stuff: finding a home, updating their mailing address, and getting a new driver’s license.

What many don’t realize is that establishing what’s called a domicile for tax purposes involves a legal dimension as well.

Understanding Domicile

You can be a resident of more than one state, but you can have only one domicile. Residency just means you live somewhere. Domicile is your permanent home; in other words, it’s the place you intend to return to and live indefinitely. It’s also what tax authorities use to determine where you owe taxes. Establishing a new domicile requires not only physically moving to your new state, but also the intent and actions you take to make it your permanent home.

Buying a home in Washington state doesn’t automatically make it your domicile if you’re still spending most of your time in your home state, still using your old driver’s license, or maintaining financial and social ties elsewhere.

Why This Matters

Your former state has a financial interest in keeping you as a resident. For that reason, tax authorities in your old state may challenge a residency change, especially when significant income or estate taxes are at stake.

When they do so, they’re not just looking at paperwork. They’re evaluating patterns: things like where you spend your time, where your doctors are, where you bank, and where you vote.

Higher tax states, such as California and New York, are notorious for doing all they can to collect revenue from former residents when documentation around domicile is unclear.

Say you retire and buy a home in Washington state, but you also keep a house in California and spend five months of the year there. California may still consider you a resident and tax you accordingly if you haven’t taken deliberate steps to establish Washington as your domicile.

However, if you can demonstrate that Washington is your one permanent home (your domicile)—through documentation, your daily patterns, and your financial ties—that could protect you from having to pay taxes in both states.

Retirees who plan to split their time between two states, or keep a home in their former state, need to be especially thoughtful about this. Keeping property in your old state isn’t a problem in itself, but it does require a clear, well-documented case that Washington is your domicile.

Proving Your Move: A Practical Domicile Checklist

Here are some practical steps to prove your change of domicile. They aren’t complicated, but taking them deliberately and documenting them carefully makes a difference.

Establishing Washington Ties

A combination of some of the following actions signal to tax authorities that Washington is your permanent home:

Get a Washington driver’s license as soon as possible after your move, ideally within 30 days.

Register to vote in Washington state.

Purchase a home or sign a long-term lease on a primary residence in Washington.

Update your mailing address with banks and financial institutions.

Establish relationships with local physicians and other medical providers.

Move your primary banking relationships to a Washington-based branch or update your address with your current bank.

Join local clubs, houses of worship, or community organizations.

Reducing Ties to Your Former State (Where Appropriate)

It’s not just about building ties in Washington; it’s also about intentionally stepping back from your old state:

Surrender your former state driver’s license when you obtain one in Washington.

Update club memberships, professional affiliations, and subscriptions to reflect your new address.

Transition your primary medical care to Washington state.

Review any property you still own in your old state and consider what role it plays in your overall plan.

Keep a “Move File”

Documenting your move is one of the most practical things you can do, and one that’s often overlooked. Keep a dedicated move file that includes:

Closing documents for your Washington home

Utility activation records

Receipts related to your relocation

A day-count log where you track the time you spend in each state

The day-count log is especially important. Many states use a 183-day rule to determine tax residency, meaning if you spend more than half the year there, they may claim you as a resident and tax you accordingly, regardless of where you say your domicile is. Keeping a simple calendar or travel log takes only a few minutes and could save you thousands in state income taxes.

Before-You-Move Financial Planning Checkpoints

Finding a new home, saying goodbye to friends, and settling into a new community can easily take center stage when you’re relocating in retirement. But it’s also important to consider some key financial decisions well before moving day—because getting the timing wrong can significantly impact your state income tax bill, either in your former state or in Washington.

Timing of Major Liquidity Events

A liquidity event is any transaction where you convert assets into cash, such as selling a business or investments, or taking a large distribution from a retirement account. If a liquidity event is in your future, the timing relative to your move deserves careful planning.

Business owners, for instance, need to weigh the implications thoughtfully. A business sale is often the largest transaction of a person’s life, and the state where you’re domiciled when that sale closes determines where you’ll need to pay income taxes on the proceeds.

If you’re planning on selling a business and relocating to Washington state around the same time, consider talking to a financial advisor and your CPA first.

Other types of transactions that require advanced planning include:

Diversification of concentrated stock positions: Selling a large block of stock in a single company could trigger Washington’s capital gains tax if the sale happens after you’ve established Washington as your domicile. If your former state has a capital gains tax or a state level income tax that applies to investment-related income, selling concentrated stock before you move may have additional tax implications— another reason to review the timing with a financial advisor and CPA before you act.

Roth conversions: A Roth conversion is when you move money from a pre-tax retirement account, like a traditional IRA or 401(k), into an after-tax Roth IRA. When you do a Roth conversion, you pay taxes on the converted amount up front, but the money grows tax-free and withdrawals in retirement are tax-free as well. Washington currently does not tax Roth conversions, but it could start in 2028 only above 1 million (see callout below).

Large charitable gifts: The tax treatment of significant donations can vary depending on your state of residence, so the timing of your gifting strategy matters, too.

Deferred compensation: Income earned in your former state but not yet received—such as a bonus, pension payout, or stock options that vest after you’ve left an employer—may still be taxable in your old state even after you’ve moved.

Investment Sales and Washington’s Capital Gains Tax

Certain long-term investment sales are subject to a capital gains tax in Washington. The state levies a 7% tax on gains between the $278,000 standard deduction and $1 million, and a 9.9% tax on gains above $1 million (2025 thresholds). Real estate sales are not subject to Washington’s capital gains tax.

If you’re planning significant investment sales, be sure to consider the timing before you establish residency in Washington state. The Washington Department of Revenue publishesguidance on the capital gains tax that’s worth reviewing. A financial advisor can also help you run the numbers to determine what makes sense for your situation.

Estate Planning Updates After Establishing Washington Residency

Moving to a new state affects more than your taxes. It can also impact the legal documents that govern what happens to your assets and who makes decisions for you if you can’t.

For instance, estate planning documents are state-specific, and documents drafted in your former state may not comply with Washington state laws. Reviewing and updating these documents after your move is an important step to protect you and your family.

Review and Re-Execute Core Documents

Wills and revocable trusts are the foundation of many estate plans. A will outlines how you want your assets to be distributed after you die. A revocable trust is similar, but with an added advantage: assets held in a trust can pass directly to your beneficiaries without going through probate. Probate is the court-supervised process of settling an estate, and it can be time-consuming and costly for your family.

Because estate planning documents must meet specific signing, witnessing, and language requirements that vary by state, an estate planning attorney will often recommend re-executing your will and trust after you move; that means signing new versions that meet Washington’s specific legal requirements.

Documents from your former state aren’t automatically invalid, but having them reviewed and reissued by a Washington estate planning attorney can remove ambiguity and avoid misunderstandings.

Update Incapacity Documents

No one likes to think about what might happen if you become incapacitated, but your durable power of attorney, healthcare directive, and HIPAA authorization are important estate planning documents.

They determine who can act on your behalf if you become unable to make decisions for yourself. Like your will and trust, these documents are governed by state laws and should be reviewed as soon as possible after your move.

Durable power of attorney: This document names someone to manage your financial affairs on your behalf if you’re unable to do so. “Durable” means it remains in effect even if you become mentally incapacitated. Washington has specific requirements for how a durable power of attorney must be signed and witnessed, so you should have any version drafted in your former state reviewed by a Washington attorney.

Healthcare directive: Also called a living will, this document records your wishes for medical treatment if you can’t communicate them yourself. It can also name someone to make healthcare decisions on your behalf. Washington’s requirements for healthcare directives differ from those in other states, so this document should be reviewed and reissued after your move.

HIPAA authorization: Without this document, your doctors are legally prohibited from sharing your medical information with anyone, including your spouse or adult children. A HIPAA authorization designates who is allowed to receive that information, and should be updated to reflect your new domicile.

Beneficiary designations are the instructions attached to retirement accounts, life insurance policies, and certain bank accounts that direct who receives those assets when you die. Regardless of what your will says, the named beneficiary receives the asset. A move is a good time to make sure your beneficiary designations are up to date and consistent with your estate plan.

Transfer-on-death (TOD) and payable-on-death (POD) designations work similarly. A TOD designation is typically attached to investment accounts or tangible assets (such as a vehicle) and allows them to bypass probate and be transferred directly to a named beneficiary when you die. A POD designation does the same for bank accounts. Reviewing these designations after your move helps ensure they still reflect your wishes and what’s in your estate planning documents.

Asset titling refers to how your property is legally owned; in other words, whose name is on it. How your home, investment accounts, and other assets are titled affects a number of things, from how they’re taxed to what happens to them when you die or become incapacitated.

Asset titling becomes particularly important if you’re relocating from a state that doesn’t have community property rules. Washington is one of only nine community property states in the country, meaning assets acquired during marriage are generally considered jointly owned by both spouses. This represents a meaningful legal shift that’s worth discussing with a Washington estate planning attorney shortly after you move.

Washington Estate Tax Awareness for New Residents

Why New Residents Often Overlook This

Many people aren’t aware that Washington has its own estate tax, separate from the federal estate tax. Many retirees relocate here from states with no estate taxes, like Florida or Texas. The federal estate tax threshold is $15 million per person, while Washington’s is $3 million.

If you’ve spent decades saving, investing, and building home equity, Washington’s estate tax may apply to you even if you’re nowhere near the federal limit.

Early Evaluation Matters

Washington’s estate tax is determined by where you’re domiciled and where you own property when you die. Adding up your assets—retirement accounts, real estate, investment accounts, life insurance benefits, and any business interests—can tell you quickly whether Washington’s estate tax is something you need to plan for.

If your net worth is approaching or above $3 million, an estate planning attorney can help you understand your options and put a plan in place to protect your family and your wealth.

Married couples should consider estate planning implications sooner rather than later. A bypass trust, for example, allows each spouse to use their own estate tax exemption. Done correctly, strategies like these may help reduce a married couple’s Washington estate tax exposure.

These structures need to be established well in advance to be effective, so the sooner you can talk to an estate planning attorney after your move, the better.

Common Mistakes Retirees Make When Moving to Washington

Even with the best intentions, mistakes happen when relocating to Washington in retirement. Here are some of the most common ones we see:

Assuming buying a home automatically establishes domicile. Having a Washington address is a start, but domicile also requires intent. That means you’ve taken documented steps to make Washington state your permanent home, like getting a Washington driver’s license or registering to vote.

Failing to track days spent in your former state. If your old state audits your residency change for tax purposes, you’ll need detailed records showing how much time you spent in your former state and your new state. Keeping a simple calendar or travel log can help document your whereabouts if questions come up.

Selling investments or a business without reviewing Washington’s tax rules first. Washington residents are subject to the state’s capital gains tax on certain investment gains and business sales. Reviewing the timing of those transactions before you move can help you avoid paying unnecessary taxes.

Not updating estate planning documents promptly after you move. Wills, trusts, powers of attorney, healthcare directives, and other estate planning documents drafted in a different state may not meet Washington’s legal requirements. Updating them as soon as you can after you move helps make sure your wishes are carried out as intended, according to Washington state laws.

Maintaining too many substantive ties to your former state. Continuing to use your driver’s license from your old state, keeping a homestead exemption, or maintaining your primary medical care there can undermine your domicile claim, even if you consider Washington home and spend most of your time here.

Moving first and planning later. If you’re moving to Washington from a higher tax state such as California or New York, there may be opportunities to defer income until after you establish domicile in Washington. For those moving from lower tax states, such as Idaho or Arizona, you may want to do the opposite. Engaging your financial planner beforethe move is best.

Moving to Washington for Retirement FAQs

What actually proves I changed my domicile?

State tax authorities look at your intent and actions in addition to your physical presence. Things like getting a Washington state driver’s license, registering to vote, seeing local physicians, updating your financial accounts, and purchasing or leasing a primary residence in Washington all build a solid case that you’ve changed your domicile. At the same time, however, you’ll need to actively reduce ties to your former state where appropriate, including surrendering your old driver’s license, canceling any homestead exemptions, and transitioning your medical care to your new state. Document everything, and keep a day-count log showing the time you’ve spent in each state. That paper trail is your best defense if your residency change is ever questioned by your old state.

Can my former state still tax me after I move?

Yes, potentially. Your former state can still tax income you earned while living there, or income tied to a business or property in that state, such as deferred compensation or bonuses earned before your move. Some states look more closely at residency status changes than others, especially when a high-income taxpayer relocates to a different state. A clear, well-documented domicile change is your best protection.

How many days do I need to spend in Washington to establish residency?

There’s no specific number of days required to establish Washington residency. Domicile is about intent and actions, not just where you live all or part of the year. That said, many states use a 183-day rule to determine whether you’re still a resident for tax purposes. If you spend more than half the year in your former state, that state may still consider you a resident regardless of where your domicile is. Carefully tracking the number of days you spend in each state is the simplest way to avoid tax disputes.

When should I update my will or trust after relocating?

As soon as possible after your move. Estate planning documents are state-specific, and a will or trust drafted in your former state may not fully comply with Washington’s state laws. An estate planning attorney can review your existing documents and recommend whether they need to be updated or re-executed in Washington. Don’t forget to update your durable power of attorney, healthcare directive, and HIPAA authorization, if needed.

Does Washington tax the sale of real estate under its capital gains tax?

No. Real estate sales are explicitly excluded from Washington’s capital gains tax. This applies to the sale of your home as well as other real estate holdings. Washington’s capital gains tax applies specifically to profits from the sale of certain long-term investments—such as stocks and bonds—and to gains from the sale of a privately held business, above the $278,000 standard deduction (2025).

If I move late in the year, how is state taxation handled?

Generally, your former state taxes income you received while living there, and Washington’s state income tax rules apply from the date you establish domicile here. Because Washington has no state income tax on wages, Social Security, pension income, or retirement account withdrawals, many retirees find that moving to Washington reduces their state income tax obligations, even if they move partway through the year. A CPA familiar with multi-state taxation can help you navigate the specifics of your situation.

Coordinated Relocation Planning: How Professional Guidance Can Help You Transition Confidently

Relocating to Washington state in retirement involves more than changing your address. The financial side of the move—including your taxes, investments, and estate plan updates—all require careful thought and coordination.

A financial advisor who specializes in retirement planning can review your domicile transition plan before major financial events, compare your state income tax implications across different timing scenarios, and work alongside your CPA and estate planning attorney to address two-state tax considerations.

If you’re thinking about making Washington your home in retirement, the sooner you start planning, the better.

Ready to Get Started?

Our team of CERTIFIED FINANCIAL PLANNER® professionals and fee-only fiduciaries based in Spokane, WA, can help. We serve clients across the U.S. or in person at our office.

We collaborate with trusted CPAs and estate planning attorneys to help coordinate the financial and legal aspects of your move so you can focus on enjoying retirement.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish. ACCEPTREJECT

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.